What is a DSCR Mortgage Loan: Understanding the Basics

When it comes to financing a real estate investment or purchasing a commercial property, understanding the various types of mortgage loans available is essential. One such type is the Debt Service Coverage Ratio (DSCR) mortgage loan. While DSCR may sound complex, it is a fundamental concept that plays a crucial role in determining loan eligibility and affordability. In this article, Simleite will delve into the basics of what is a dscr mortgage loan, explaining what it is and how it works to provide a solid foundation of knowledge for borrowers and investors.

What is a DSCR Mortgage Loan: Understanding the Basics

A DSCR mortgage loan is a financial tool that assesses the income-generating capacity of a property relative to its debt obligations. Understanding what is a dscr mortgage loan is crucial for borrowers and investors in the real estate market. By comprehending how DSCR is calculated, its interpretation, and its impact on loan eligibility, borrowers can make informed decisions and navigate the mortgage loan process more effectively. While what is a dscr mortgage loan have their advantages, borrowers should also consider other factors and metrics involved in the loan evaluation process. Overall, a solid understanding of DSCR empowers borrowers to explore financing options and make informed choices when investing in real estate.

- Defining DSCR:

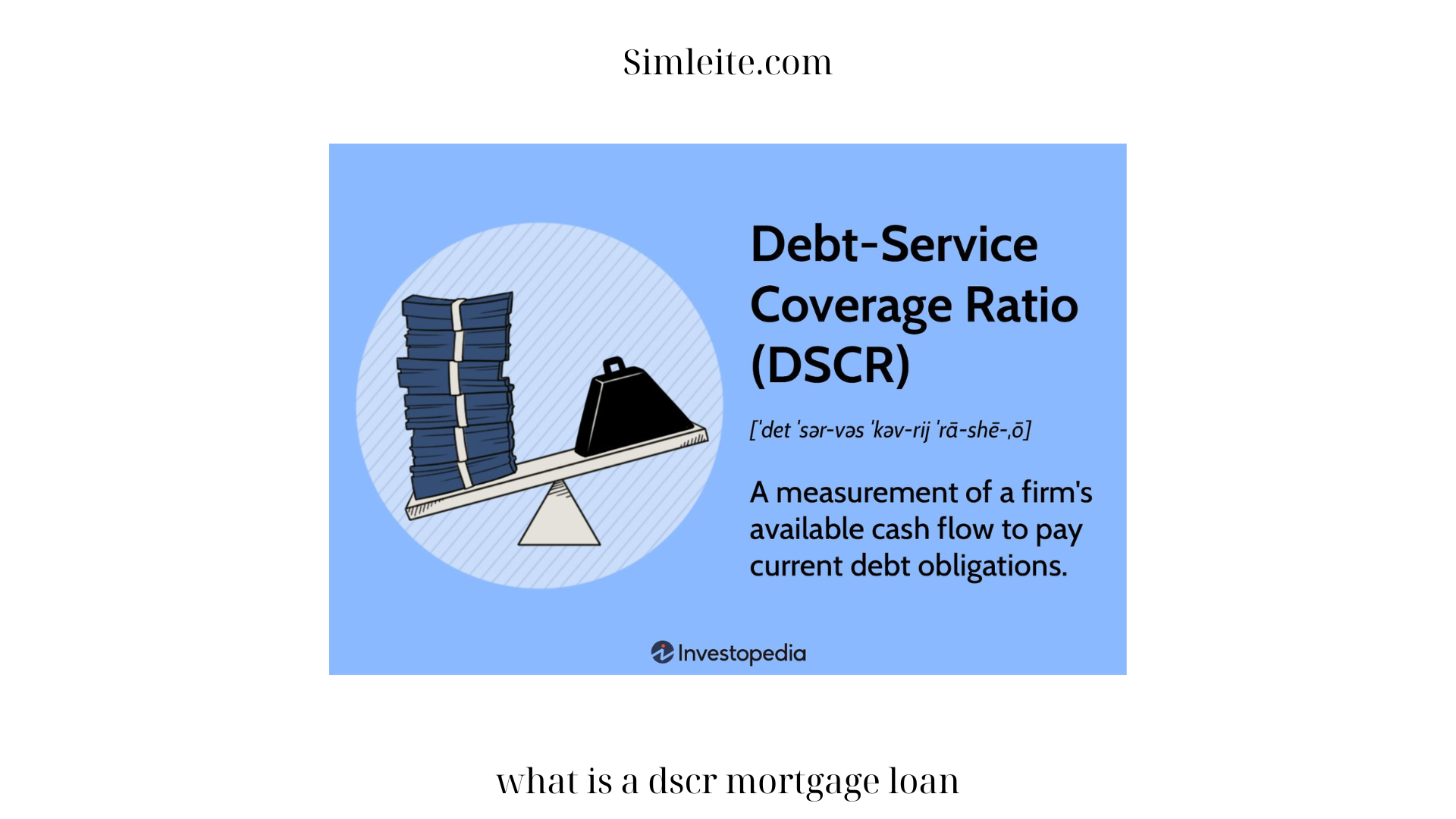

Debt Service Coverage Ratio (DSCR) is a financial metric used by lenders to assess the borrower’s ability to generate sufficient income to cover the loan’s debt service obligations. It is a ratio that compares the property’s net operating income (NOI) to the total debt service, including principal and interest payments. In simple terms, DSCR measures the property’s cash flow relative to its debt obligations. - How DSCR is Calculated:

To calculate what is a dscr mortgage loan, divide the property’s net operating income by the total debt service. Net operating income represents the property’s rental income minus operating expenses, excluding debt service. Total debt service includes principal and interest payments on the mortgage loan. The resulting ratio indicates the property’s ability to generate enough income to meet its debt obligations. - Interpreting DSCR Values:

DSCR values can range from less than 1 to greater than 1. A DSCR below 1 indicates that the property’s cash flow is insufficient to cover its debt obligations, suggesting a higher risk for lenders. On the other hand, a DSCR above 1 signifies that the property generates more income than required to cover its debt payments, indicating a lower risk for lenders.

- Importance for Lenders:

Lenders use the what is a dscr mortgage loan as a risk assessment tool when evaluating mortgage loan applications. A higher DSCR demonstrates a property’s strong cash flow and its ability to generate income to repay the loan. Lenders typically prefer borrowers with higher DSCR values, as it reduces the risk of default and increases the likelihood of timely loan repayments. - Impact on Loan Eligibility:

The what is a dscr mortgage loan plays a significant role in determining loan eligibility. Lenders typically have specific DSCR requirements that borrowers must meet to qualify for a DSCR mortgage loan. The minimum required DSCR varies depending on factors such as the type of property, the lender’s risk appetite, and prevailing market conditions. Meeting the lender’s DSCR criteria is crucial for borrowers seeking approval for a mortgage loan. - Factors Affecting DSCR:

Several factors influence the what is a dscr mortgage loan of a property. These include rental income, operating expenses, vacancy rates, interest rates, and loan terms. Higher rental income, lower operating expenses, and lower interest rates contribute to a higher DSCR. Conversely, factors such as high vacancy rates, increasing operating expenses, and rising interest rates can lower the DSCR. - Advantages of DSCR Mortgage Loans:

DSCR mortgage loans offer several advantages for borrowers. Firstly, they provide a clear assessment of a property’s income-generating potential and its ability to cover debt obligations. This transparency helps borrowers make informed decisions regarding property investments. Secondly, DSCR mortgage loans can be helpful in financing commercial properties, as they focus on the property’s cash flow rather than the borrower’s personal income. - Limitations and Considerations:

While what is a dscr mortgage loan have their advantages, borrowers need to be aware of their limitations and considerations. Since DSCR primarily assesses the property’s income-generating capacity, borrowers with strong personal income but weaker property cash flow may face challenges in qualifying for these loans. Additionally, DSCR mortgage loans may have stricter underwriting requirements and higher interest rates compared to traditional residential mortgages. - Alternative Metrics:

In addition to DSCR, lenders may consider other metrics when evaluating mortgage loan applications. For instance, Loan-to-Value (LTV) ratio assesses the loan amount relative to the property’s appraised value. Personal credit history, borrower’s experience, and market conditions may also be taken into account. It is important for borrowers to understand the specific criteria and metrics used by lenders when applying for a mortgage loan.

- Conclusion:

What is a dscr mortgage loan? It is a financial tool that assesses the income-generating capacity of a property relative to its debt obligations. Understanding what is a dscr mortgage loan is crucial for borrowers and investors in the real estate market. By comprehending how DSCR is calculated, its interpretation, and its impact on loan eligibility, borrowers can make informed decisions and navigate the mortgage loan process more effectively. While DSCR mortgage loans have their advantages, borrowers should also consider other factors and metrics involved in the loan evaluation process. Overall, a solid understanding of DSCR empowers borrowers to explore financing options and make informed choices when investing in real estate.